Despite the worst housing crisis since the Great Depression, owning a home is still central to the hopes and aspirations of many Americans. Even with the recent decline in house prices, owning a home can bestow more financial and non-financial benefits than any other single asset. This means more economic mobility and financial security for families, and stronger communities too.

As this chapter explains, the shift away from standard mortgage loans and strong underwriting during the 1990s and early 2000s, along with a fractured regulatory environment, sparked the foreclosure crisis and economic meltdown. New mortgage reforms in the Dodd-Frank Act and efforts of the Consumer Financial Protection Bureau and state regulators will help ensure this disaster does not reoccur. At the same time, there is a strong need to prevent even more foreclosures and ensure that the rebuilt mortgage market preserves access to credit for families who could be successful homeowners.

Overview [Video]

CRL Senior Researcher Debbie Bocian covers the key findings in the "Mortgages" chapter of State of Lending.

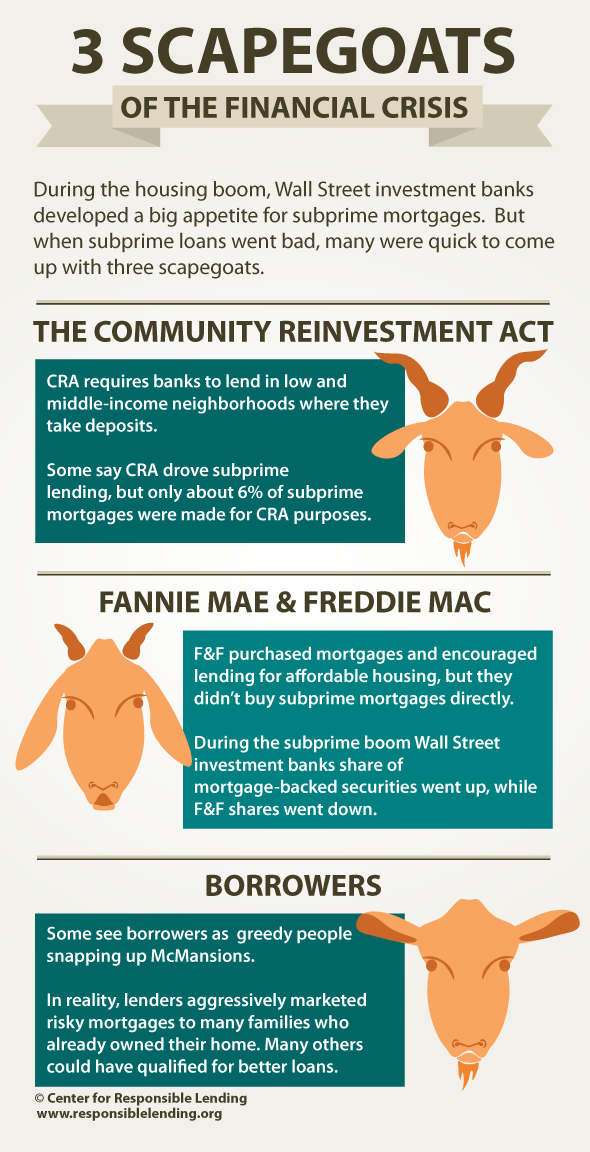

The Three Scapegoats [Infographic]

Ever since the financial crisis started, the Blame Game has been a popular pastime. In this infographic, we highlight players who often get more than their share of pointing fingers.