The debt collection industry is a rapidly expanding business, with revenue increasing up to 600 percent between 2003 and 2012. Private companies buy billions of dollars of charged-off debt from banks each year. The most common type of debt purchased comes from credit cards, but debt buyers also buy student loans, medical debt and more.

As the industry has grown, abuses and illegal — predatory — practices have proliferated. Companies are using abusive and unlawful methods to collect on debt — too often on debt that the targeted consumers do not even owe. This chapter covers how the industry frequently operates on inaccurate and incomplete information, resulting in dire financial consequences for consumers.

- In the U.S., more than 1 in 7 adults is being pursued by debt collectors. The average amount of debt is $1500.

- In 2013, the Federal Trade Commission (FTC) received over 200,000 complaints about debt collection—the highest number of complaints on any topic other than identity theft.

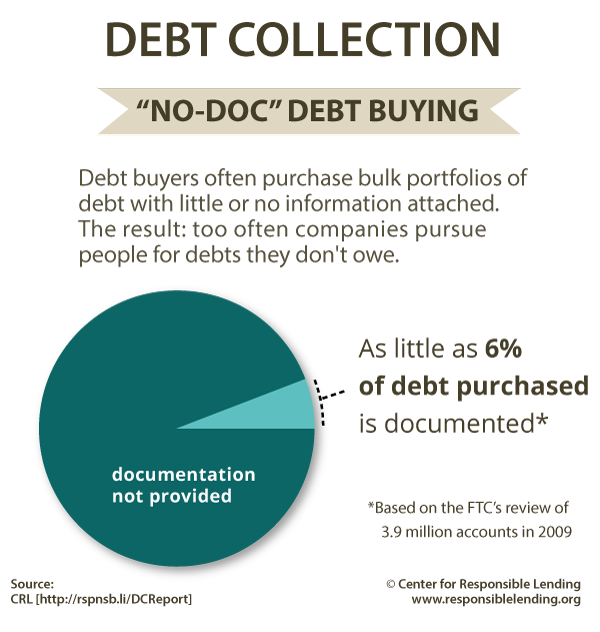

- According to an FTC analysis, only 6 percent of debt accounts purchased by some of the largest debt buyers in 2009 came with any documentation.

- Overwhelmed courts make the problem worse by awarding judgments to debt buyers based on false, forged, or misleading information.

Federal banking regulators, including the Consumer Finance Protection Bureau, can and should clean up an industry that is out of control. This report includes specific recommendations for holding banks accountable for the debts they sell, and for strengthening consumer protections on the state and federal levels.

Percent of "No-Doc" Debt [Graphic]

Debt buyers often purchase bulk portfolios of debt with little or no information attached. The result: too often companies pursue people for debts they don't owe.

5 Things to Know About Debt Buying & Collection

Here are a few essential facts for understanding how the growing debt industry operates and the negative impact on consumers. Available as [PDF].